Credit scoring service in Qatar Credit Bureau is a system that assesses an individual's creditworthiness based on various factors such as their credit history, outstanding debts, payment patterns, and the overall financial behavior. It helps financial institutions and lenders in Qatar to evaluate the risk associated with extending credit to individuals. By using this service, lenders can make more informed decisions when considering loan applications, credit card approvals, or other financial services. The credit scoring service ultimately aims to promote responsible borrowing and lending practices while ensuring a fair and transparent system for all parties involved.

Product Overview

Credit Scoring Mark issued by Qatar Credit Bureau is an indicator to the possibility of a customer's default over a period of time.

The Credit Scoring Mark is ranged from 300-850, where the largest number indicates a lower risk level.

The numerical score reflects your level of repayment commitment. The higher your score, the better your credit behavior is considered to be.

The following table illustrates the credit scoring marks:

Indicates a strong credit history and a high level of repayment commitment.

Reflects a good level of commitment and stability in credit behavior.

Indicates an acceptable level of commitment, with room for improvement in credit behavior

Reflects the presence of credit behavior concerns that may affect the customer’s overall

Indicates a weak credit history and a higher level of repayment-related risk.

Factors influencing credit scoring

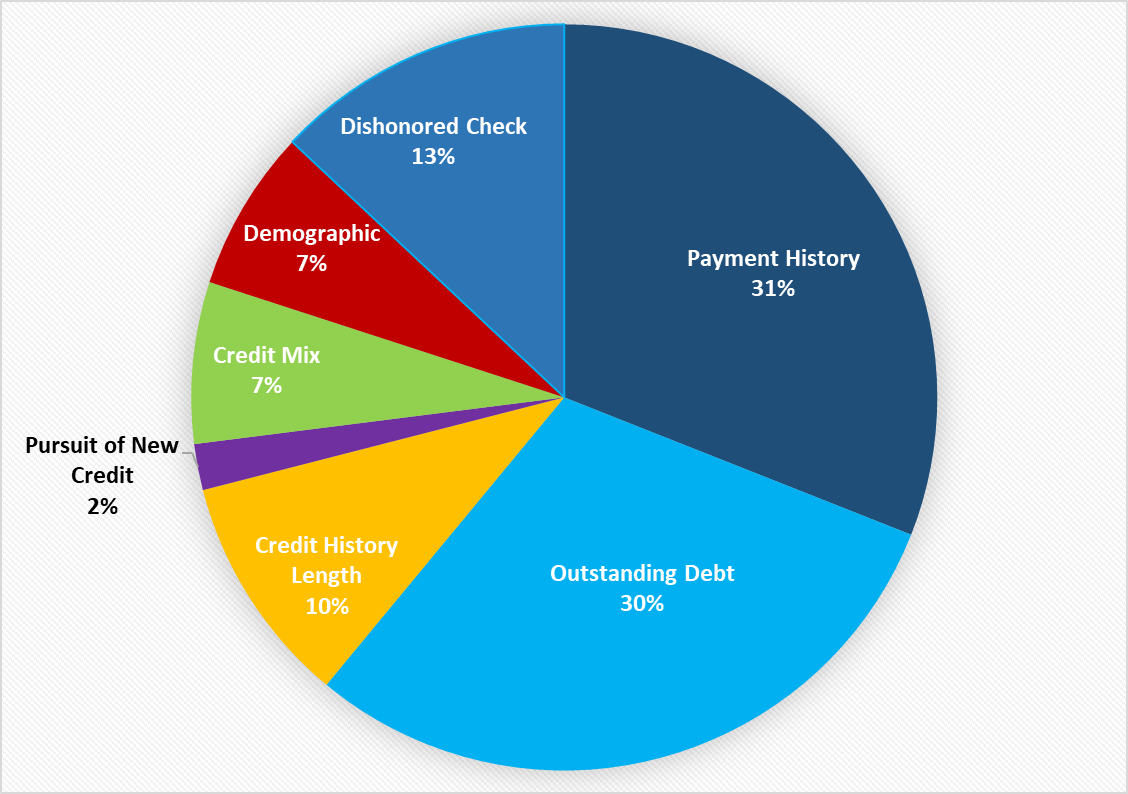

The following pie chart shows the factors influencing credit scoring of individuals and the percentage of each factor:

Explanation of Credit Scoring factors:

1- Payment history (31% of your score)

The extent to which you meet your credit repayment obligations on time.

2- Outstanding Debt (30% of your score)

The level of credit utilized compared to your available credit limit.

3- Length of credit history (10% of your score)

The duration for which you have maintained credit facilities.

4- Credit mix (7% of your scores)

The diversity of your credit facilities and your consistency in repaying

them.

5- New credit (2% of your score)

The number of credit applications or inquiries related to opening new

credit facilities.

6- Demographic (7% of your score)

General information used as part of the credit scoring models.

7- Dishonored Cheques(13% of your score)

The number of returned cheques associated with you and how recent they

are.

Credit Score Improvement Guidelines:

1. Make Payments on Time

Consistently paying your financial obligations on time helps improve your credit score and demonstrates a high level of financial discipline.

2. Maintain an Appropriate Level of Credit Obligations

Keeping your credit utilization at a reasonable level can improve your credit score and reflect balanced financial management.

3. Review Your Credit Report Regularly

Regularly reviewing your credit report helps ensure the accuracy of the information recorded and allows you to address any issues that may affect your credit score.

4. Limit Multiple Credit Applications Within a Short Period

Submitting several credit applications within a short timeframe may indicate a higher level of risk and could negatively impact your credit score.

Qatar Credit Bureau provides data, information, and analysis only, and

does not participate in or influence decisions regarding the approval or rejection of credit applications.